How Labour’s benefit cuts cost the poorest renters thousands of pounds

The cost of living measure that must be a non-negotiable for the next prime minister

As the government wrestles with the coming inflation spike, there’s a simple move that hasn’t been talked about much. It’s not cheap. But it is necessary.

That move is to reverse Labour’s housing benefit cuts. If you weren’t aware of “Labour’s housing benefit cuts”, that tells you how well this has been reported. But yes, Labour’s housing benefit cuts.

In both her Budgets, Rachel Reeves froze the cash value of the Local Housing Allowance (LHA). LHA places a cap on the housing benefit paid to private renters on the lowest incomes, and freezing its cash value while rents go up means cutting its “purchasing power”.

In this post, “housing benefit” includes both old-style Housing Benefit (note the capitalisation) and its replacement, the Universal Credit housing element.

Government data reveals:

more than 175,000 low-income tenants face a shortfall on their rent as a result of Labour’s housing benefit cuts

a further 900,000 low-income tenants face larger rent shortfalls than before

renters who two years ago would have had their rent fully covered by housing benefit must now find thousands of pounds a year

in some parts of England hardly any private rents are fully covered by housing benefit, especially for single childless under-35s

I’ve been writing about LHA cuts for years, but explaining how it works doesn’t get any simpler. So this time I’m getting someone else to do it.

Margot Robbie in a bathtub explains the Local Housing Allowance

LHA sets an upper limit on the housing benefit paid to the poorest privately renting tenants. It’s based on how many bedrooms the tenant needs, plus geography – the government looks at a large sample of new and renewed private sector rents in each “broad rental market area” (BRMA), and sets LHA at the 30th percentile of those rents, so that 30% of local private rents for that property size are fully covered by housing benefit.

For example – take a low-income couple in Bournemouth with a 12 year old daughter and a six year old son. According to government rules, they need three bedrooms. The government looks at over a thousand new and renewed private sector rents for three-bedroom properties in the Bournemouth BRMA, and identifies the 30th percentile – the point at which 30% of those rents are lower, and 70% are higher.

That comes out at £310.68 a week – roughly £16,155 a year. If the parents rent a home for up to that amount, their entire rent is covered by housing benefit. But if they rent a more expensive home, their housing benefit only covers that £310.68 a week – they must pay the shortfall themselves.

Get it? Good. Anyway this bathwater’s getting cold, so I’ll hand you back.

Margot sips more champagne, blankly ponders the meaning of life, the bathwater slowly gets colder

So long ago, Oliver Dowden was still a thing

Thank you Margot – you’ve now served your penance for Wuthering Heights.

So now you know how LHA works. But there’s a problem – the LHA freeze.

LHA last rose in April 2024. But even those 2024 LHA rates were based on rental data collected between October 2022 and September 2023 – that’s the time lag in the system – which, combined with Labour’s freeze, means that current housing benefit caps are based on the 30th percentile of rents from three years ago, as if rents magically haven’t risen since then.

But they have, of course. Let’s take that Bournemouth family. That 30th percentile figure – £310.68 a week – is what the LHA rate would be now had Labour not frozen it. But because Labour did freeze it, the actual maximum housing benefit they can claim is the LHA rate from April 2024, based on rents from way back in late 2022 and 2023 – which is £264.66. That’s £2,393 a year lower.

And it means that instead of fully covering the cheapest 30% of privately rented three bedroom homes in Bournemouth, it only covers the cheapest 12%.

A Labour government – a Labour government…

We can see this effect across the country. The percentage of claimants across England, Scotland and Wales whose private sector rent is fully covered by housing benefit fell from 52% in May 2024 – just after LHA last rose – to 43% in January 2026, the most recent figures available.

The number of housing benefit claimants facing a rent shortfall rose by 175,822 in that time, reaching a total of 1,075,724 this January, even though the overall number of claimants barely changed.

That means 175,000 low-income tenants have to make up rent shortfalls as a direct result of Labour’s cuts – and 900,000 tenants who already faced shortfalls (because their rent was always higher than the cheapest 30% locally) have seen those shortfalls get substantially bigger.

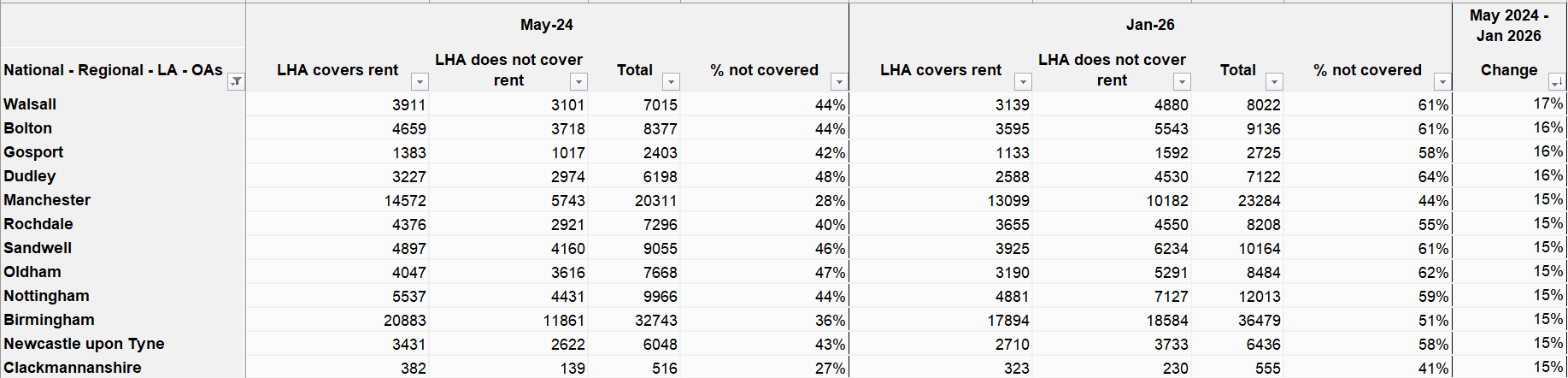

Certain areas have been particularly affected, especially the West Midlands and Greater Manchester. The share of tenants whose Universal Credit housing element doesn’t fully cover their rent has risen by 17% in Walsall – from 44% in May 2024 to 61% in January 2026 – by 16% in Bolton, Dudley and Gosport in Hampshire, and by 15% in Manchester, Birmingham, Rochdale, Oldham, Sandwell, Nottingham, Newcastle, and Clackmannanshire in Scotland.

In fact, eight of Greater Manchester’s ten boroughs have seen a rise of 13% or more. Little wonder that late last year, regional mayor Andy Burnham – now preparing to challenge for the Labour leadership – joined calls to raise LHA rates.

How much is this costing tenants? The short answer is “lots”. The longer answer involves looking at each property size, based on the number of bedrooms.

Using government data for England, we can see the average shortfall faced by tenants paying the 30th percentile of local market rents – in other words, the gap between the rent they’re paying and the housing benefit they receive under the frozen LHA rate:

one bedroom in shared accommodation (aka the “shared accommodation rate”): average £754 annual shortfall

one-bedroom property: £1,206

two-bedroom property: £1,566

three-bedroom property: £1,875

four or more bedrooms: £2,412 (£2,190 excluding the Central London BRMA)

Those are big numbers on low incomes – or on average incomes for that matter. All things being equal, these tenants would have had their rent fully covered two years ago (except in parts of London where national housing benefit caps bite), but must now make up four-figure shortfalls.

And the impact is even worse in some areas. Let’s take the shared accommodation rate. This is particularly important because most single, childless under-35s are restricted to this rate, which is based on renting a single room in a shared property. The annual shortfall between the current 30th percentile rent and the frozen LHA cap is more than £2,000 in Reading and Inner South West London (basically Wandsworth). And it’s more than £1,000 in a further 38 BRMAs in England, mostly strewn across London and southern England, but also including Southport, Birmingham, Leeds, Bolton and Bury, Tameside and Glossop, and Central Greater Manchester.

For self-contained one-bedroom homes, 15 areas have shortfalls of more than £2,000, nearly all in London but also including Reading again. There are 32 such areas for two-bedroom homes, mostly in London and the south east but also in Greater Manchester, while 40 areas have shortfalls above £2,000 for three-bedroom homes.

It can’t get worse, can it?

Take a wild guess….

All this has reduced the stock of private rented housing that is affordable with housing benefit. Thirty percent of privately rented housing is supposed to be fully covered by housing benefit, but the actual rental figures – the raw data from October 2024 to September 2025 that was meant to determine this year’s LHA rates – show that across England:

on average, 12% of one-bedroom shared housing in each BRMA is now fully covered by housing benefit

11% of one-bedroom housing

11.5% of two-bedroom housing

14% of three-bedroom housing

16% of four+ bedrooms

To be clear, this is based on the benefit that’s paid for each type of accommodation – If your household is deemed to need two bedrooms, you can’t claim the three-bedroom LHA cap.

In four areas – Maidstone, East Cheshire, Chichester and Worcester North – the government didn’t record a single shared accommodation rent in its sample that is fully covered by the frozen LHA rates. What percentage of local shared housing rents are fully covered by LHA in these areas? Looking at the data, basically zero.

There are 60 areas where less than ten percent of shared accommodation rents are fully covered by LHA, spread right across the country from the tip of Cornwall to Teesside, from the Kent coast to Kendal. The corresponding figure for one-bed housing is 53 areas; 50 areas for two-bed housing; 24 areas for three-bed; and 19 areas where less than ten percent of the biggest rental homes are fully covered by LHA.

Ok ok I get it, it’s bad

I could throw even more stats at you, but by now you get the picture. Tenants whose rent remains below the frozen LHA cap haven’t suffered any benefit cuts yet, but there are less of those tenants every passing month that rents rise and LHA remains frozen.

Why is this happening? Obviously the driver is money – but also politics, in my view. LHA freezes aren’t even announced – they just emerge when it turns out that each new Budget hasn’t accounted for LHA uprating and it transpires it’s been frozen again. There’s no legislation, parliamentary vote or formal announcement that might spark a backlash, and media coverage is focused on the Budget’s headline announcements. Other than obsessives (like me), it just gets lost in the noise.

I think housing activists are a bit half-hearted in calling for higher housing benefit as “it just goes to landlords”.

This is the sibling of the trope that higher housing benefit just leads landlords to raise rents. The Tories cut housing benefit in real terms year after year during the 2010s, arguing that LHA had simply given landlords free rein.

“LHA has now run its unaffordable course and we must turn it around,” former welfare secretary Iain Duncan Smith said in defence of LHA cuts in 2010. “It fuelled a landlords’ charter to raise rents and has made housing more expensive for the whole population.”

But the subsequent decade of LHA cuts did not see rents fall. Private rents barely shifted in relation to incomes between 2012 and 2020, including for those on lower incomes.

Ultimately if you want to push down private rents you need to weaken the bargaining power of private landlords through a combination of mass housebuilding, renters’ rights and possibly rent control (an argument I’ll leave for another day). Cutting housing benefit doesn’t work. It was never going to.

How much would reversing Labour’s housing benefit cuts cost? £1.5bn a year and rising, according to the Institute for Fiscal Studies (IFS). It’s not gigantic by the standards of government spending, but it’s not cheap either.

There’s two points to be made here. First, this is the Treasury’s own fault. Every time the Treasury (and these days it is the Treasury) decides to freeze LHA, it knows full well that eventually those cuts will have to be reversed and the link to the 30th percentile restored – just as it was in 2020 and 2024 after previous multi-year freezes – and that this will cost money. Labour’s LHA freeze doesn’t even have a purported rationale – it’s just opportunistic penny-pinching.

Second, this is the fastest-acting measure the government can take to address housing affordability as living costs rise. Its impact is more immediate than renters’ rights, which require individual tenants to pursue legal action to enforce, or a rent freeze, which would require consultation and legislation. Housebuilding is needed but takes years.

Reversing the LHA cuts won’t help everyone, but it will benefit the million or so low-income claimants who face rent shortfalls, even where it merely serves to reduce their shortfall rather than erase it.

Cutting housing benefit is a road Labour should never have gone down, having opposed it while in opposition and knowing full well where it leads. By the next Budget we’ll almost certainly have a new prime minister and probably a new chancellor too. If they don’t reverse this cut, it will be a strong sign that nothing has really changed.